FINMA Circular 2016/7: QES Exemption Removed, Non-Bank Transfers Out

FINMA's partial revision of Circular 2016/7 removes the special treatment of the qualified electronic signature route and excludes non-bank payment service providers as secondary-verification counterparties. Firms running either channel in KYC onboarding will need to rebuild before the final Circular takes effect.

Dr. iur. Servatius von Tatzenberg

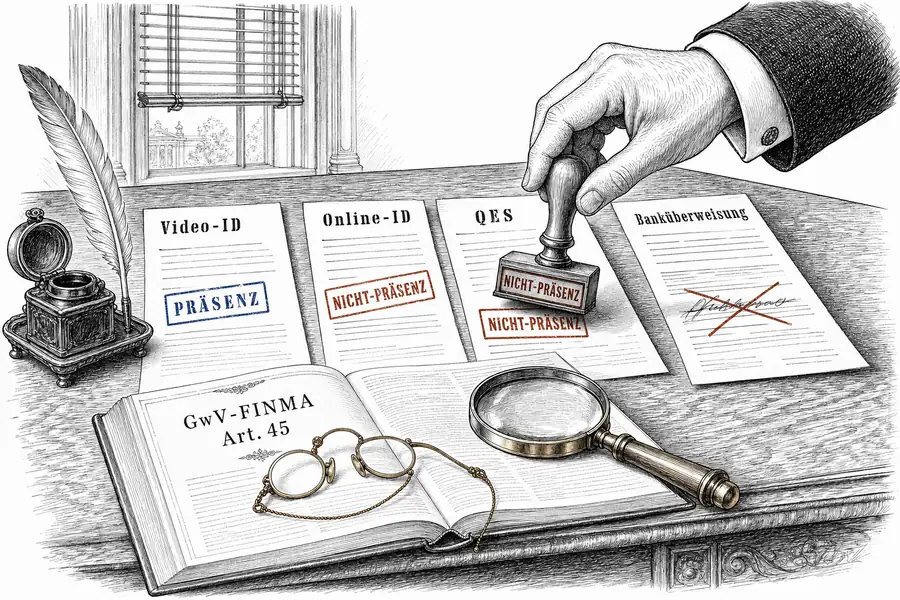

FINMA opened the consultation on the partial revision of Circular 2016/7 “Video and Online Identification” on 16 December 2025; the period runs until 27 February 2026. The draft aligns the Circular with the Federal Act on Electronic Identity Documents (BGEID), which enters into force in mid-2026, and removes two special-treatment provisions: the qualified electronic signature (QES) route loses its exemption from the residential address requirement; non-bank payment service providers are excluded as counterparties for secondary verification. The residential address check under Art. 45(2) GwV-FINMA remains the operational pivot.

Video identification with a live operator remains equivalent to in-person identification. Machine-readable zone, two security features — the existing verification sequence holds. Identification documents bearing a QR code alongside the MRZ are now also accepted. Firms that have invested in this channel retain that investment.

Online identification without live audio was already classified as non-face-to-face business under the current Circular; the revision changes nothing in that regard. It clarifies and expands the methods for the residential address verification required under Art. 45(2) GwV-FINMA: cross-checking against postal and address databases, registry lookups, documentary proof via utility or tax bills, or — new — geolocation of the end device at the time of transmission. The choice of verification method is modular; the verification step itself is mandatory.

The QES route loses its special status. The qualified electronic signature under ZertES — permissible as a remote signature since the 2022 ordinance revision (Art. 7(1) ZertES-V) — previously carried an exemption: no secondary verification, no separate residential address confirmation. The draft reclassifies it as non-face-to-face business and requires the same residential address verification under Art. 45(2) GwV-FINMA as any other online channel. Art. 3(2) GwV-FINMA preserves FINMA’s discretion to grant technology-based derogations — a foothold for a proportionality submission, provided the firm can identify a concrete question on which its own standard takes a position. Firms that relied on this exemption for fully digital onboarding flows should build in a residential address verification step before the final Circular takes effect.

Bank transfer as secondary verification remains permissible, now also in the reverse direction with a code sent to the customer’s account. The counterparty must be a regulated financial intermediary subject to supervision comparable to Switzerland’s. PayPal, card issuers, and other non-bank payment service providers are excluded. Any firm using such a transfer for identification purposes under Art. 45 GwV-FINMA will need to rebuild that channel.

The e-ID under BGEID becomes a valid identification document. FINMA accepts it as a full alternative to physical identity documents, provided the document’s validity and the holder’s attribute assignment are verified. The residential address check remains a separate requirement: the BGEID attribute does not satisfy it.

The revised Circular applies only to financial intermediaries supervised by FINMA; casinos and licence holders under the Federal Act on Gambling, as well as certain operators under the Precious Metals Control Act, are excluded.

Before 27 February, firms should map two internal paths: QES onboarding still relying on the old exemption, and secondary verification routed through non-bank payment service providers. For firms with high QES volume, a consultation response is worthwhile if the firm can identify a concrete proportionality question under the Art. 3(2) GwV-FINMA discretion. Which of the available residential address verification methods is operationally viable is a question each firm’s compliance architecture will answer once the final Circular is in hand.

The open question is the third-country dimension: how narrowly will FINMA interpret “comparable supervision” for non-Swiss banks? The answer will follow after the consultation responses are evaluated and the final Circular is published.